The following are the latest ratings and target prices for US stocks from various brokerage firms:

Huatai Securities Maintaining Horton House (DHI.N) Buy rating:

The company's FY25 results were under pressure, with revenue of $34.25 billion (down 7% year-on-year) and net profit of $3.59 billion (down 25% year-on-year), mainly due to declining volume and prices as well as rigid costs. However, Q4 net sales turned positive year-on-year, and inventory control and improved turnover enhanced operational resilience. In a rate-cutting cycle, highly affordable products are expected to benefit first. Strong cash flow and share buybacks and dividends demonstrate the company's ability to return value to shareholders. Based on a P/TBV of 2.13x, the target price is $178.

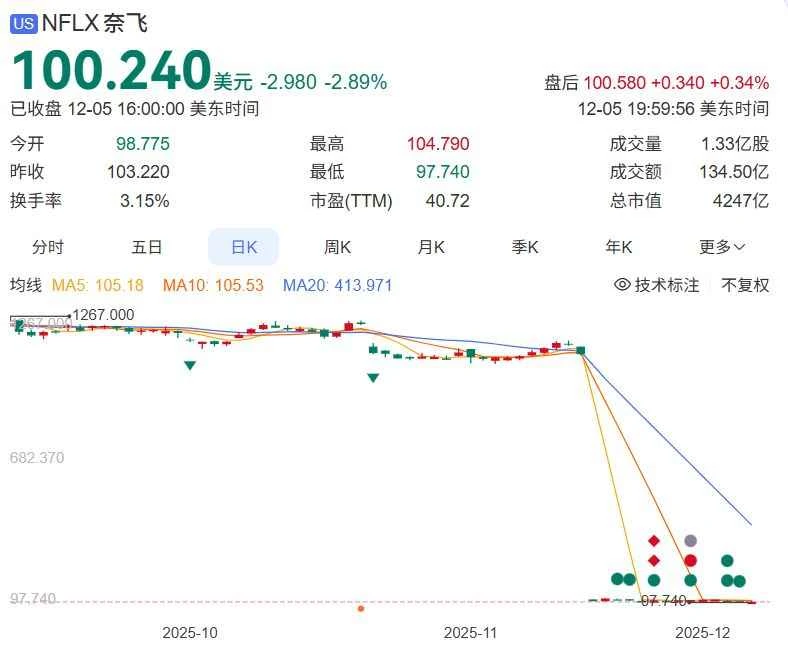

CITIC Securities Maintaining Netflix (NFLX.O) Hold rating:

3Q25 revenue met expectations, with high-quality content driving user growth. Games like "Wednesday Season 2" and "K-Pop Devil Hunter" performed exceptionally well. Advertising revenue and user experience optimization contributed to long-term growth. Operating profit was affected by a one-off Brazilian tax, but performed well excluding this. Current valuation already reflects optimistic expectations; attention should be paid to earnings realization and the progress of new businesses.

China International Capital Corporation Maintain Tianhong Technology (CLS.N) Buy rating, target price $360:

The company's Q3 2025 results slightly exceeded expectations, benefiting from the increased proportion of high-margin HPS business and strong demand for 800G switches. AI ASIC server orders are expected to enter mass production in 2027, coupled with CCS business revenue growth exceeding 40%, strengthening future growth certainty. Capacity expansion and technological leadership build competitive barriers. We raise our 2026 target PE to 40x and our target price to $360.

Guojin Securities Maintain Buy rating on Tianhong Technology (CLS.N):

The company achieved high growth in both revenue and profit in Q3 2025, driven by AI in its data center business . Strong network demand solidifies the leading position of Ethernet white-box switches. CCS business is experiencing rapid growth, with 102.4T switches expected to drive further growth in 2026. While the enterprise market faces short-term pressure, a turning point is approaching; Non-GAAP EPS guidance has been raised to $5.9, with long-term benefits expected from the expansion trends in AI inference and ASICs.

CICC maintains Visa's (VN) Outperform rating, target price $400:

4QFY25 results exceeded expectations, with net revenue up 11.5% year-over-year, driven by a recovery in payment transactions. Cross-border transactions increased by 17%, and customer incentives met expectations. Although operating expenses are under short-term pressure, FY26 guidance is solid, with EPS growth at a "low double digit." Current valuation is below target, share buybacks and dividends enhance shareholder returns, and long-term competitiveness remains strong.

CICC maintains its position on New Oriental (EDU.N) Outperform rating, target price $69:

1QFY2026 revenue met expectations, while non-GAAP operating profit exceeded expectations, benefiting from contributions from Oriental Selection and the resilience of the study abroad business. Continued cost reduction and efficiency improvement led to a 1 percentage point year-on-year increase in operating profit margin to 22.0%. We have raised our FY26/27 earnings forecasts for education. New business growth is accelerating, strengthening shareholder returns. The target price is based on FY26 SOTP, with the core business PE ratio revised upward from 12x to 14x to reflect a valuation premium.

CICC maintains Mondelez International's (MDLZ.O) Neutral rating, target price $70:

3Q25 results met expectations, with revenue up 5.9% year-over-year, but European profits were under pressure as cocoa costs peaked. North American biscuit demand remained weak, with significant consumer divergence. We lowered our 2025 EPS forecast to $2.90, while maintaining our 2026 forecast at $3.290. The long-term growth outlook remains unchanged, and current valuations have some room for recovery.

Huatai Securities maintains Nvidia's (NVDA.O) Buy rating, target price $245:

Blackwell and Rubin GPUs have raised their order guidance to $500 billion for the next five quarters, far exceeding expectations. Revenue and net profit forecasts for FY26-28 have been revised upwards, benefiting from AI factories, HPC, communications, and robotics. Ecosystem expansion. The company dominates cloud computing power and extends its reach to industry, biology, autonomous driving, and quantum computing, building a comprehensive AI layout and solidifying its leading position.

(Article source: CLS)