On September 10th, Eastern Time, [the company] announced a $300 billion artificial intelligence [project] with OpenAI. Following the large order, Oracle , a long-established American technology giant The stock price surged by more than 40% intraday, reaching a record high of $345.22, which briefly propelled founder Larry Ellison to the top of the world's richest list.

However, less than two months later, Oracle's stock price has fallen to $243.8, a cumulative drop of 29.6% from its previous all-time high. The $251 billion (approximately RMB 1.78 trillion) market capitalization that surged due to the $300 billion deal has been almost entirely wiped out, and the previous celebrations of investors have vanished like a dream.

Meanwhile, the credit market is issuing increasingly sharp alarms for Oracle : Oracle's credit default swaps (CDS) have risen to 87.7 basis points—the highest level in nearly 18 months.

This dramatic fluctuation not only indicates that institutional investors are becoming increasingly cautious about Oracle's credit prospects, but also forces us to ponder whether the bubble behind the artificial intelligence boom is already on the verge of collapse.

Oracle's trillion-dollar market value evaporates

On September 10, Eastern Time, Oracle, a US tech giant, surged 36% in a single day, with its market value soaring by $251 billion (approximately RMB 1.78 trillion), shocking global investors and causing a frenzy among many tech stocks on Wall Street.

The surge in Oracle's stock price is directly attributable to a major deal it recently signed with OpenAI: a five-year, $300 billion computing power procurement contract starting in 2027. This contract not only far exceeds OpenAI's current revenue but is also one of the largest cloud contracts in history.

OpenAI's purchase of 4.5 gigawatts (GW) of computing power from Oracle is roughly equivalent to the current capacity of a data center in operation in the United States. A quarter of that computing power is equivalent to the electricity generated by more than two Hoover Dams, or the electricity consumption of about 4 million households.

However, as the initial excitement of these dizzying numbers faded, growing concerns about an AI bubble began to emerge. Oracle's credit default swaps (CDS) have been steadily increasing since early September.

Oracle's CDS has nearly doubled since August, rising from about 40 basis points to nearly 88 basis points, a dramatic increase achieved in just over two months. This means that credit concerns surrounding Oracle are intensifying at the fastest pace since 2024.

This data shows a significant shift in market sentiment towards Oracle.

In the first three quarters of 2025, Oracle's credit default swap (CDS) trading prices fluctuated steadily between 30 and 45 basis points. Then, in September, CDS began to climb, breaking through 60 basis points by the end of the month and further rising to 80 basis points in October. In early November, this level peaked at 87.735 basis points—the highest level since mid-2024.

This sharp acceleration suggests that traders are rushing to hedge their positions, foreshadowing a sudden reassessment of Oracle's creditworthiness.

Why did market sentiment suddenly shift?

So, what caused this sudden change? Several factors seem to be working together:

1. Rising borrowing costs: High U.S. Treasury yields have significantly increased refinancing costs for all corporate borrowers, including large technology companies.

Second, large-scale infrastructure spending increased leverage: Oracle's aggressive expansion into cloud infrastructure and artificial intelligence data centers has temporarily increased its leverage ratio.

III. Industry-wide Concerns: On Amazon and Microsoft The cautious guidance from companies has exacerbated the credit crunch across the technology sector, amplifying hedging activities surrounding technology debt.

IV. Expected Pricing: Credit default swap traders often react before actual credit events, sometimes causing excessive volatility during periods of uncertainty.

Deeper concerns

Behind the surge in Oracle CDS, the most fundamental concern is that investors are beginning to realize that, despite the national-level investment commitments behind these AI infrastructure procurement contracts, the foundations supporting these commitments seem shaky.

Or to put it more bluntly, the current boom in investment in the artificial intelligence industry seems to stem from an "ouroboros" cycle: hyperscale data centers sell computing resources to infrastructure models, the infrastructure models feed back usage to cloud platforms, and suppliers lock in "future" revenue in advance—the operation of this entire process depends on the increasing amount of non-traditional credit.

This model works perfectly when free cash flow is sufficient to cover all expenses. But once cash flow slows and the bills shift from retained earnings to financing contracts, the model fails—and that could be the moment the bubble bursts.

What will happen next?

Of course, we cannot say that the artificial intelligence bubble will burst immediately, nor can we say that Oracle's CDS spread of nearly 90 basis points necessarily means that the company will default—but it does reflect the market's increased expectations of volatility.

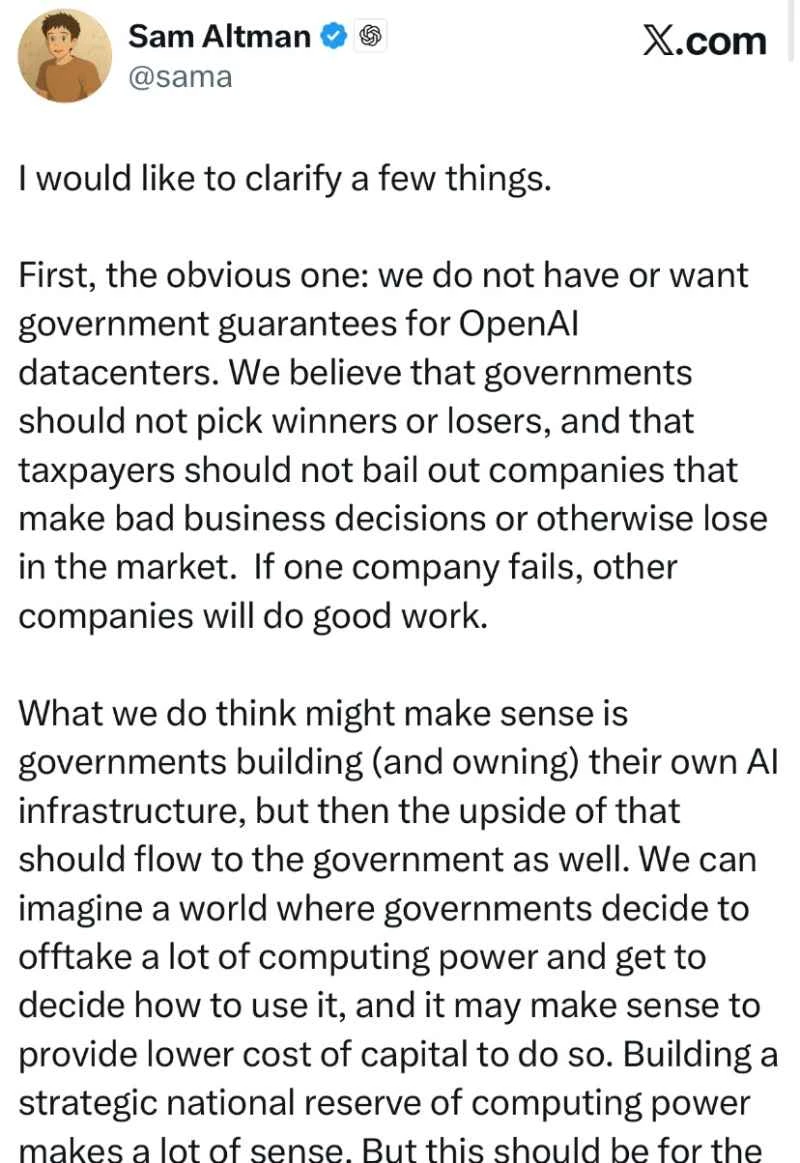

On Wednesday, OpenAI CFO Sarah Friar publicly stated that the company is seeking to build a system powered by banks. An ecosystem comprised of private equity funds and federal government backstops or guarantees to help companies finance their massive chip investments has undoubtedly heightened concerns about an AI bubble.

Although Friar and OpenAI CEO Altman both posted clarifications on Thursday, concerns about an AI bubble are unlikely to dissipate.

As global stock markets dance to the tune of the AI craze, more and more people are eagerly listening and waiting to see when the final note of this liquidity dance will sound.

(Article source: CLS)