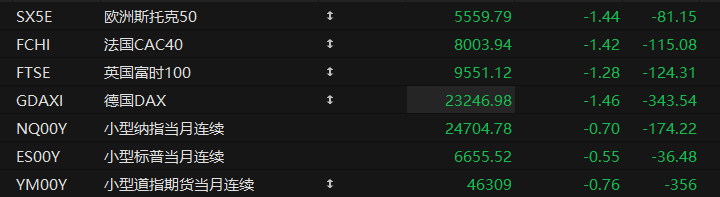

With the rise of Google's seventh-generation TPU, the demand for HBM may continue to grow.

According to reports from South Korean media outlets such as the Chosun Ilbo, Samsung Electronics and SK Hynix have become key players in Google's TPU supply chain. SK Hynix is reportedly poised to become the preferred supplier of the 8-layer HBM3E chip for Google's seventh-generation TPU and will exclusively provide the 12-layer HBM3E chip for the improved seventh-generation TPU (TPU 7e), enabling it to achieve higher energy efficiency.

KB Securities The report suggests that Google's expansion of its AI ecosystem through TPUs could increase memory supply at Samsung Electronics' advanced foundry and improve its capacity utilization. The report notes that Google's seventh-generation TPUs are expected to use HBM3E, while the eighth-generation TPUs are expected to use HBM4, thus Samsung Electronics' HBM supply next year will more than double compared to the previous year.

Analysts at South Korean investment and securities firms predict that SK Hynix will account for 56.6% of Google's HBM supply in TPUs this year, while Samsung Electronics will account for 43.4% . Meritz Securities, however, believes that SK Hynix's market share will reach 60%.

Previously, the HBM market had always revolved around Nvidia. GPUs currently dominate the market, but the emergence of TPUs may disrupt this landscape. Similar to GPUs, each TPU integrates 6-8 HBM modules, therefore, the expansion of TPUs will directly determine future HBM demand. In addition to TPUs, Korea Investment & Securities points out that companies from Meta and Amazon... AWS's custom chips are also expected to drive growth in the HBM market.

The growth in HBM demand is expected to continue to drive up DRAM prices. KB Securities stated that in 2026, demand for DRAM used in servers will increase by 35% compared to the previous year, but supply will only increase by a maximum of 20% , meaning that the upward trend in prices may intensify.

Based on the above trends, DRAM and NAND Flash manufacturers are gradually shifting their focus from simply expanding production capacity to upgrading process technology, high-level stacking, hybrid bonding, and high-value-added products such as HBM.

According to TrendForce, DRAM capital expenditure is projected to reach $53.7 billion in 2025, and is expected to grow further to $61.3 billion in 2026, representing a year-on-year increase of approximately 14%. NAND Flash capital expenditure is projected to reach $21.1 billion in 2025, and is expected to grow slightly to $22.2 billion in 2026, representing a year-on-year increase of approximately 5%.

Guojin Securities It is pointed out that AI is driving a rapid increase in storage demand, but storage manufacturers' capital expenditures have not yet entered an expansion cycle. Currently, the industry's cleanroom space is nearing its limit, and among major DRAM manufacturers, only Samsung and SK Hynix still have limited room for expansion. Even if capital expenditures are revised upwards, the increase in capacity in 2026 will be limited.

Given the limited increase in new production capacity, Zhongtai Securities The report indicates that driven by the explosive growth in demand for AI inference, the storage market is expected to experience a tight supply and demand situation throughout 2026. Currently, in addition to price increases in mainstream DRAM and NAND, niche storage technologies such as DRAM, 2D NAND (including SLC and MLCNAND), and NOR Flash have all seen price hikes since Q3 2025. This super-cycle in storage has driven a significant improvement in the profitability of storage companies starting in Q3, and it is expected that profitability will continue to improve as prices rise further.

Dongcai Illustrated Guide: Some Useful Tips

(Article source: CLS)