There are indications that a large transaction occurred in the U.S. interest rate market late last week, seemingly setting the stage for the Federal Reserve's upcoming announcement of the end of its balance sheet reduction program (i.e., quantitative tightening, QT).

Data from the CME Group shows that a large trade involving 40,000 November-expiring contracts occurred last Thursday, betting that the November secured overnight funding rate (SOFR) would average less than 9 basis points higher than the expected federal funds rate.

Analysts point out that this trade would mark a shift in the trends of both this year and reflects growing expectations that the Federal Reserve will announce the end of the QT policy at the end of its policy meeting on Wednesday.

Data shows that the SOFR is currently 4.24%—this rate is the overnight lending rate for short-term cash primarily secured by Treasury bonds, reflecting the funding cost in the overnight repurchase market. The federal funds rate is currently 4.11%—this rate is the rate set by banks... Unsecured overnight lending costs charged between parties to meet reserve requirements.

Traders pointed out that the aforementioned 40,000 contracts mean that a 1 basis point change in the interest rate spread would result in a profit or loss of approximately $2 million. This measure of interest rate risk is known as "DV01".

Given that the risk exposure of this transaction is almost entirely concentrated on the spread of the one-month interest rate, the size of this position can be described as extremely large—its interest rate sensitivity is equivalent to holding $2 billion to $3 billion in 10-year Treasury bonds.

Essentially, the trade is betting that if the Federal Reserve announces a reduction in its quantitative tightening program at its two-day meeting this week and implements a 25-basis-point rate cut as expected, the November SOFR average rate will fall to 3.95% or lower, while the federal funds rate will be at 3.86% (4.11% - 0.25%) or higher.

This contrasts sharply with expectations in the forward market – one-month forward contracts on Friday showed that traders expect SOFR to be 10 basis points above the federal funds rate by the end of November, which would be a record spread level, indicating that repo funding conditions remain tight.

Deutsche Bank US interest rate strategist Steven Zeng said this is a bet that the Federal Reserve will halt QT this week and announce new policies to appease funding markets, which would narrow the SOFR spread relative to the federal funds rate from its current level. He stated, "Although CPI is still at 3%, the latest inflation data we received last week was slightly lower than expected."

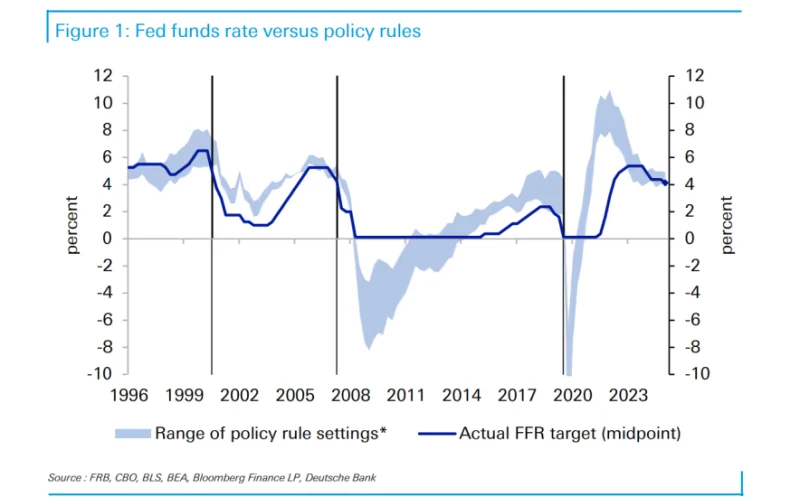

Federal Reserve Chairman Jerome Powell stated on October 14 that the Fed is prepared to end QT, citing reasons including tightening liquidity conditions and stronger repurchase rates.

The end of QT will lead to lower repurchase rates.

Generally speaking, periods of quantitative tightening (QT) by the Federal Reserve often coincide with rising repurchase rates , because when Treasury bonds and agency securities... When the debt matures, the Federal Reserve will not reinvest the proceeds. Instead, the U.S. Treasury will redeem the debt and pay the Federal Reserve by deducting the required amount from its cash deposit account (TGA) balance at the Federal Reserve.

To replenish its cash balance, the U.S. Treasury must issue more new debt. Investors will then use funds in their bank accounts to purchase these new bonds, which in turn lowers bank reserve levels. With fewer available cash or reserves for overnight lending, banks and money market funds exert upward pressure on repurchase rates.

However, the situation will clearly reverse when the balance sheet reduction ends. As the Federal Reserve reinvests maturing securities , the downward trend in bank reserves will stop and may even rebound, thereby increasing system liquidity and leading to a decrease in repurchase rates.

The rise in repurchase rates over the past few months has also stemmed from the U.S. Treasury's aggressive issuance of short-term Treasury bonds to replenish cash reserves following the lifting of the debt ceiling in the summer. The surge in Treasury issuance has increased market demand for repurchase financing.

Jonathan Cohn, head of U.S. interest rate strategy at Nomura Securities, now shares the view of Zeng, a strategist at Deutsche Bank , that the driving force behind the aforementioned spread trade between SOFR and the federal funds rate lies in the potential dynamics of the Federal Reserve's balance sheet.

He also pointed out that the market generally expects the Federal Reserve to likely "provide liquidity support by injecting reserves back into the system or lowering the interest rate on liquidity release operations."

Since mid-October, the SOFR rate has hovered near the upper limit of the Federal Reserve's 4.00%-4.25% policy rate range, even briefly exceeding this range twice. Going back further, since August 22, the SOFR rate has consistently been higher than the federal funds rate, and remained higher for most of the year.

In fact, ideally, the SOFR rate should be lower than the federal funds rate —because the former is backed by Treasury bonds and has extremely low credit risk. In contrast, the federal funds rate reflects unsecured interbank lending and involves counterparty risk. Therefore, lenders in the federal funds market typically demand a slightly higher rate than the SOFR to compensate for this risk.

However, this unusual inversion in the US interest rate market recently undoubtedly highlights the shift in power in the short-term funding market.

Of course, not all market participants believe that these large transactions stem from bets on the end of QT. Jan Nevruzi, U.S. interest rate strategist at TD Securities, believes that the CME Group's large transactions may not be solely driven by balance sheet reduction. He argues that they reflect the valuation expansion seen throughout the year, suggesting that investors may be "selling at high levels."

Dongcai Illustrated Guide: Some Useful Tips

(Article source: CLS)