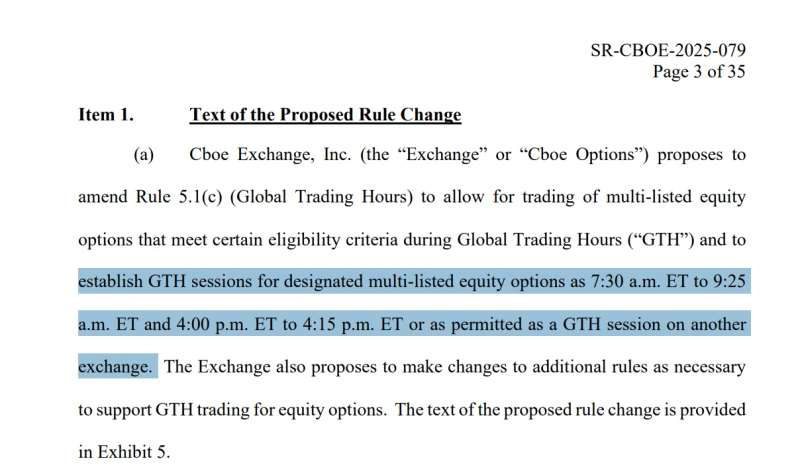

The following are the latest ratings and target prices for US stocks from various brokerage firms:

CITIC Securities Maintain Overweight rating on DoorDash Inc-A (DASH.O) with a target price of $232.

The company's Q3 2025 revenue reached $3.45 billion (YoY +27.3%), with a record high monetization rate and a GAAP net margin of 1.0%. In 2026, the company's strategy focuses on AI, autonomous driving, and overseas expansion. Increased capital expenditure may put short-term pressure on the company, but its long-term competitive advantages are expected to strengthen. Based on future growth potential, a target price of $232 is given.

CITIC Securities maintains its "Buy" rating on Gitlab Inc-A (GTLB.O):

The company's revenue and seat growth exceeded expectations this quarter, benefiting from the technological advantages of the DevOps platform and increased activity in the open-source community. We are optimistic about the medium- to long-term growth momentum driven by the shift to the left in security and the widespread adoption of microservices and containerization; however, in the short term, we remain cautious in our guidance due to the impact of weak SMB customer demand and the risks posed by AI.

China International Capital Corporation We maintain our neutral rating on Palantir Technologies Inc-A (PLTR.O) with a target price of $150.

The company's Q3 2025 results exceeded expectations, with revenue increasing by 63% year-on-year and GAAP net profit reaching $4.77 billion. Growth was driven by AI products in the commercial sector, with US commercial revenue increasing by 120% year-on-year, net retention rate improving to 134%, and TCV increasing by 151% year-on-year. The profit model has been optimized, with the Rule of 40 exceeding 100. We have raised our 2025/26 revenue forecasts, with a target price corresponding to 37x 2028E EV/Sales.

CITIC Securities maintains its "Buy" rating on Shopify Inc-A (SHOP.O):

3Q25 results exceeded expectations, driven by accelerated international expansion and merchant promotion, and enhanced AI capabilities boosting omnichannel sales. The company's leading position remains solid, benefiting from macroeconomic resilience, cost reduction and efficiency improvement, and the implementation of AI applications. Expansion into large enterprise clients, B2B, offline, and international businesses opens up long-term growth potential.

CITIC Securities maintains its buy rating on Spotify Technology SA (SPOT.N):

The company's revenue and profit in Q3 2025 exceeded expectations, benefiting from price increases, improved gross margins, and cost control; the guidance for Q4 2025 met expectations. Global expansion and increased ARPU are driving growth, while content cost optimization and cost reduction continue to release profits. The company possesses strong resilience and broad long-term growth potential.

SPDB International maintains its support for BeiGene. (ONC.O) Buy rating, target price $390:

Benefiting from strong sales of zanubrutinib (exceeding $1 billion in a single quarter) and improved operational efficiency, Q3 2025 results exceeded expectations. The company raised its revenue guidance and lowered its expense guidance, with profitability continuing to improve. R&D is progressing smoothly, with multiple hematologic oncology products having intensive catalyst development; Sonrotoclax and BGB-16673 have best-in-class potential. Based on the upward revision of earnings forecasts and DCF valuation, the target price is raised to $390.

CICC maintains its position on Beike (BEKE.N) Outperform rating, target price $25:

Q3 2025 revenue met expectations, while adjusted net profit exceeded expectations, benefiting from cost control. Existing property GTV increased by 5.8% year-on-year, with improved profitability in the home improvement and rental businesses. Although we have lowered our 2025-26 earnings forecasts, we remain optimistic about the platform's competitiveness and medium- to long-term earnings potential. Our target price is based on a 2026 non-GAAP P/E of 30x, representing a 55% upside from the current 19x.

Guohai Securities Give to Duolingo (DUOL.O) Overweight rating:

The company's Q3 2025 revenue reached $270 million (YoY +41%), with adjusted EBITDA of $80 million (YoY +68%), exceeding expectations. However, Q4 earnings guidance was lowered, and the strategic focus shifted to long-term user growth, putting pressure on short-term profits. We are optimistic about the LTV growth and long-term potential driven by improved teaching quality, but given the slowdown in short-term growth, we have lowered our 2026-2027 earnings forecasts and maintain our "Buy" rating.

CITIC Securities gave Qualcomm (QCOM.O) Buy rating:

The company's quarterly results exceeded expectations, benefiting from growth in its high-end Android, automotive, and IoT businesses. Despite Apple's... While its baseband market share declined, the company successfully expanded into new products and completed an acquisition in the industrial IoT sector, entering the high-growth data center market. The company secured its first order in the sector. Its diversified portfolio strengthens growth support and demonstrates significant long-term investment value.

CICC maintains Monster Beverage (MNST.O) Outperform rating, target price $73:

3Q25 results exceeded expectations, benefiting from the global boom in energy drinks, smooth price increases in the US, a clear new product strategy, and strong international growth. We have revised our EPS forecast upwards, with the valuation shift reflecting the category premium. We are optimistic about market share growth and the innovation cycle expected in 2026.

CICC maintains its position on Autohome (ATHM.N) Neutral rating, target price $29:

The company's Q3 revenue and profit slightly exceeded expectations, thanks to cost control. Traditional advertising and lead generation businesses faced pressure, but new retail... Revenue from other businesses increased by 32.1% year-on-year, including new energy. Revenue related to automobiles increased by 58.6%. The company is advancing its O2O ecosystem closed loop, has ample cash reserves, and continues to repurchase shares and distribute dividends. The target price is based on a non-GAAP P/E ratio of 15.9x for 2026, representing a 19% upside from the current price.

CICC maintains its controlling stake in Gas Energy. (CELH.O) Neutral rating, target price $50:

3Q25 results met expectations, with revenue of $725 million (up 173% year-over-year), driven by strong growth from the Alani Nu brand. Market share in the US increased to 20.8%, reflecting healthy retail trends. Although PepsiCo lowered its 2026 EPS forecast to $1.51, [the company's performance was positive] . Channel support is expected to boost Alani sales. The target price is based on a 2026 P/E ratio of 33x, representing a 20% upside. Risks: Lower-than-expected repurchase rates, intensified competition.

CICC maintains its position on Yage Technology (YALA.N) Outperform rating, target price $10.3:

3Q25 results exceeded expectations, with both revenue and profit increasing, mainly due to games. In-app purchases increased and cost control was optimized. Flagship product promotions drove record revenue, while new games gradually contributed incremental growth. Non-GAAP net profit was revised upward by 3%, with P/E ratios of 9/8 times for 2025/2026, making the valuation attractive. Share buybacks continued, improving shareholder returns, and we are optimistic about the medium- to long-term outlook.

Huatai Securities Maintain NetEase Youdao (DAO.N) Buy rating, target price $12.75:

The company's advertising, AI subscription, and high school business drove growth. In Q3, it benefited from increased spending in the gaming industry and AI product iterations, leading to accelerated cash collection. The adjustment of its literacy-related business is nearing completion, and revenue is expected to return to positive growth. Non-GAAP net profit continues to improve, SOTP valuation is reasonable, and long-term growth is promising.

(Article source: CLS)