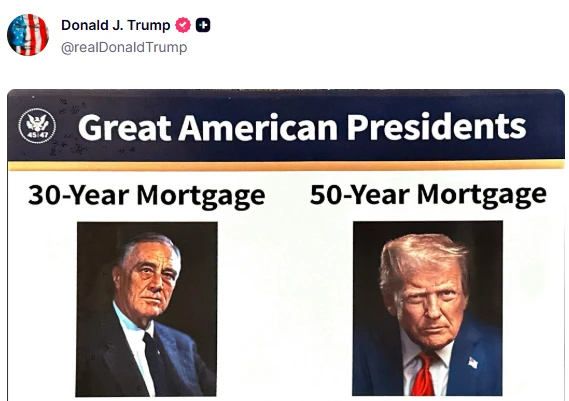

To make homeownership more affordable, US President Trump came up with a "new idea" last week—planning to introduce 50-year mortgages to help Americans more easily realize their "homeownership dream." However, as soon as this plan was announced, many mortgage analysts rushed to issue warnings, suggesting that the White House should proceed with caution…

Trump's post about the product on his Truth Social media platform last weekend quickly caused a stir in the United States. Bill Pulte, head of the Federal Housing Finance Agency, which oversees Fannie Mae and Freddie Mac, responded that they are "working on it" and stated that it will "completely change the game. " rule".

Clearly, a major objective of the Trump administration's attempt to extend mortgage terms is to reduce homebuyers' monthly payments—the longer the loan term, the less principal needs to be repaid each month.

In recent years, rising home prices and mortgage rates have significantly reduced the affordability of homeownership for the average American, leaving many potential homebuyers unable to afford mortgage payments. Some homebuyers have begun turning to variable-rate mortgages to reduce monthly payments, and long-term mortgages (up to 50 years) may offer them another option.

However, this approach also has other significant drawbacks. The most direct cost is that homebuyers will incur significantly higher interest payments over the entire loan term, and their home equity accumulation will be much slower…

Will it never end before he dies?

The potential operational methods and calculations for a 50-year mortgage are as follows:

Let's assume a $400,000 home with a 20% down payment and an existing mortgage rate of 6.22% (Freddie Mac's projected rate for a 30-year mortgage last week). If the homebuyer chooses a 50-year mortgage, their monthly principal and interest payments will be about $200 less than with a 30-year mortgage. However, over the entire loan term, the homeowner will ultimately pay about $335,000 more in accumulated interest than with a 30-year mortgage—almost equal to the home's current value.

The above estimates are based on the premise that the interest rate for a 50-year mortgage is the same as that for a 30-year mortgage.

But this will clearly be difficult to achieve in the future – Guggenheim Securities Co-Chairman Jim Millstein stated that lenders are likely to charge higher interest rates to offset the credit risk associated with the additional 20-year term, as borrowers may default during this period. Ultimately, the higher interest rates could offset most, or even all, of the savings on monthly payments.

Meanwhile, homeowners with 50-year mortgages will accumulate home equity much slower than those with 30-year mortgages , because the longer repayment period primarily involves paying interest. Even assuming the same interest rate, if a 50-year mortgage holder sells their home after 10 years, their home equity will be approximately $38,000 less than that of a 30-year mortgage holder. This does not include property taxes and insurance payments made over those ten years. Expenses and maintenance costs.

Other drawbacks include the additional 20-year repayment period, which means that major life events (such as divorce or unemployment) could make repayment difficult.

Even considering that the median age of first-time homebuyers in the United States has climbed to a record 40, a 50-year mortgage term means that many people may never be able to pay off their loans and will instead pass the debt on to the next generation...

“This will lead to the intergenerational transfer of debt rather than wealth assets,” noted Pete Carroll, director of public policy and industry relations at Cotality.

In fact, for many American homebuyers, the down payment, rather than the mortgage, may be the biggest obstacle. Extending the loan term does nothing to help. Jordan Levine, chief economist at the California Association of Realtors, points out that if 50-year mortgages successfully stimulate housing demand, it may actually drive up prices and increase the burden on homebuyers.

Financial risks cannot be ignored

Laurie Goodman, founder of the Center for Housing Finance Policy at the Urban Institute, a Washington think tank, said that many questions remain unanswered regarding 50-year mortgages, including how investors in mortgage-backed securities will view the product…

The Federal Housing Finance Agency (FHFA) currently regulates Fannie Mae and Freddie Mac, the two largest mortgage lenders. Fannie Mae and Freddie Mac do not issue loans themselves; instead, they acquire approximately half of all U.S. home loans from lending institutions, package and sell them to investors, and provide repayment guarantees for these loans.

It is worth mentioning that private lending institutions in the United States had previously tried such ultra-long-term mortgage loans, especially in the years leading up to the 2008-09 financial crisis.

For example, Fannie Mae began offering 40-year mortgages in 2003 and expanded the program in 2005. It wasn't until 2014 that the Federal Housing Finance Agency prohibited Fannie Mae and Freddie Mac from purchasing loans with terms exceeding 30 years.

Millstein, who served as the U.S. Treasury’s chief restructuring officer from 2009 to 2011, pointed out that “there were many similar so-called innovations before the financial crisis that were designed to reduce mortgage costs, but they ended up being a disaster.”

Some analysts say that to support 50-year mortgages, Trump will need Congress to repeal the law prohibiting government-guaranteed loans with terms exceeding 30 years. TD Cowen analyst Jaret Seiberg stated that while regulators could approve 50-year mortgages themselves, the process would take a year or more.

Joel Berner, senior economist at Realtor.com, wrote in a statement: "This (50-year mortgage) is clearly not the best way to solve the housing affordability problem. The best thing the government can do is to reverse the inflation caused by tariffs, which is pushing up the interest rates on existing mortgages."

Conservative Republican Representative Marjorie Taylor Greene also explicitly opposed the idea of introducing 50-year mortgages, arguing that such mortgages would make banks... Mortgage lenders and homebuilders profit, but ordinary Americans pay significantly higher interest rates, sometimes dying without ever having paid off their mortgages…

(Article source: CLS)