On December 5th, a piece of news that shook the global film and television industry was officially released.

streaming giant Netflix Warner Bros. Discovery announced it will acquire Warner Bros. Discovery for approximately $82.7 billion (including debt, with a total equity value of approximately $72 billion, or $27.75 per share). WBD (World Business Development & Research) is the film and television production business of HBO, as well as its streaming platform HBO Max.

This is not only the largest merger and acquisition deal in Hollywood in recent years, but it may also reshape the entire entertainment industry landscape.

Under the agreement, WBD will retain its traditional businesses, including its cable television network, news, and sports channels, and spin them off into a new publicly traded company called "Discovery Global." Netflix's acquisition of Warner Bros. includes franchises such as *Harry Potter* and * Game of Thrones*. It includes classic IPs such as Friends, as well as core film and television assets such as the DC Universe and HBO original series.

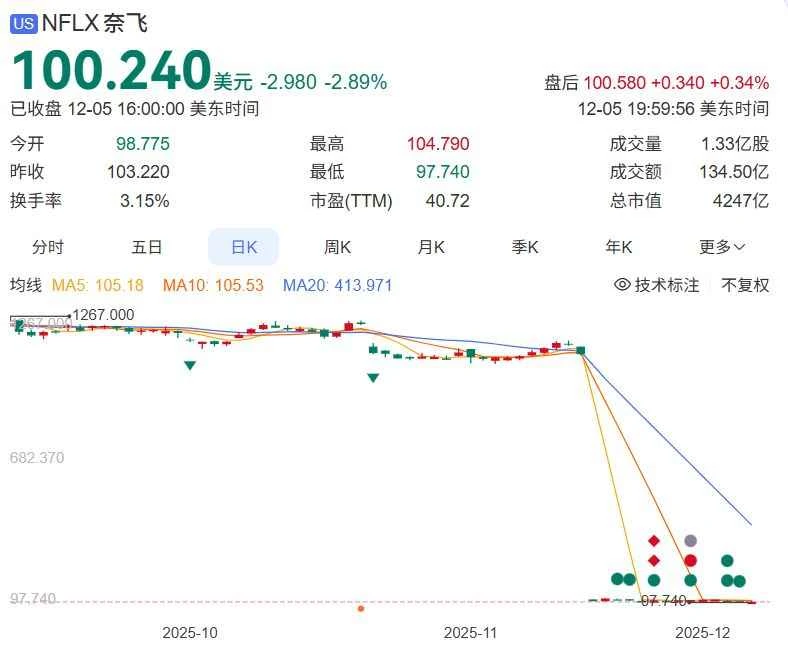

Netflix daily candlestick chart

The market reaction to the announcement was mixed. Netflix shares fell 3.5% to 4% in pre-market trading, reflecting investor concerns about the debt burden and integration challenges of the massive deal. On the other hand, WBD shareholders received a bid of $27.75 per share, significantly higher than the previous market price, representing a dignified and profitable exit.

Warner Bros. explores daily candlestick chart trends

As a "tech streaming giant," Netflix has always been considered to lack the qualities of Disney. With such a strong IP foundation, the industry generally believes that this transaction is not an ordinary merger and acquisition, but a key point for Netflix to completely leap from a streaming service provider to a studio-level giant.

Jin Ge (pseudonym), who has long been involved in film and television investment in Hollywood, told a reporter from the Daily Economic News: "Netflix is making up for its weakest point, otherwise it risks being left behind by the entire industry."

What does Netflix really want after acquiring Warner's core assets for a huge sum?

WBD has been undergoing a difficult transformation over the past few years.

With cable TV subscribers continuing to decline and competition in the streaming media market intensifying, the company has repeatedly attempted to stem the bleeding through internal restructuring. One key initiative was to separate content production and streaming services from the traditional cable TV network into two independent companies, in order to reduce the burden and focus on the core business.

It was against this backdrop that Netflix became involved in the bidding war.

Netflix's official platform account announced the acquisition of WBD. Image source: Netflix.

It is understood that Paramount, Comcast, and others Several companies, including Netflix, had expressed interest, but Netflix ultimately won with a combination of cash and stock. More importantly, it not only offered a higher total price but also promised that WBD shareholders would hold both Netflix stock and shares in the newly formed Discovery Global, making it more attractive in terms of long-term value.

Of course, this deal is not without risk. The agreement includes a hefty "breakup fee" clause, meaning Netflix would have to pay billions of dollars in damages if the deal falls through due to regulatory or other reasons. Furthermore, WBD must complete the divestiture of its cable television assets before the formal closing, adding further uncertainty to the process.

Jin Ge believes that Netflix's move is not primarily driven by "ambition," but rather by a need to "catch up." "The lack of content is no secret within Netflix. It used to rely on blockbuster shows to drive growth, but the competitive landscape has changed. Disney has Marvel and Star Wars, Universal has the 'Fast & Furious Universe,' and Amazon..." And Apple Everyone's throwing money at it. Only Netflix doesn't have its own 'super content engine.'

While Netflix has maintained its leading position in the global streaming market over the past few years, sluggish growth and a slowdown in subscription growth have become real challenges. Without a continuous stream of competitive content, user retention and attracting new users will be limited.

In Jin Ge's view, this acquisition is to some extent a "defensive offense." If Netflix doesn't fill the gap in its IP portfolio, it already faces the risk of being marginalized.

However, if successful, Netflix will no longer be just a content distribution platform, but will truly possess the complete capabilities of a top Hollywood studio, from script development and filming to theatrical distribution and streaming.

Hollywood has entered an oligopoly era; how can small and medium-sized players survive?

This deal is significant for much more than just "Netflix's content library has grown." It marks the arrival of a new era: streaming platforms are no longer content buyers or customizers, but are directly controlling the source of content production.

In the past, Netflix's model was clear: spend money to buy copyrights, invest in producing original series, and then use algorithms to precisely target global users. However, the lack of a traditional studio background meant a kind of "disconnect" between it and theaters and traditional distribution channels. Now, having acquired Warner Bros., a Hollywood giant with a century-long history, it will have access to countless classic IPs, a mature production team, and a global distribution network.

To truly understand the significance of Netflix's move, it's helpful to look at the major Hollywood acquisitions that have shaped the industry over the past decade. In fact, since the rise of streaming media, giants have been engaged in an arms race to acquire content, intellectual property, and studios. So where does Netflix's $82.7 billion investment stand?

Compiled by NBD reporter based on publicly available information

Data shows that the last deal of similar size was Disney 's $71.3 billion acquisition of 21st Century Fox in 2019. That deal laid the content foundation for Disney+ and was also seen as a key move by traditional giants to fight back against streaming media.

Netflix's latest deal is not only more expensive but also more focused on pure film and streaming assets, excluding non-core businesses such as news or sports. While AT&T acquired Time Warner for approximately $85 billion in 2018, that was an attempt by a telecommunications company to integrate media across sectors, and it included a large number of non-entertainment assets such as CNN. In contrast, the Netflix-WBD deal is a truly content platform-driven "precise takeover" of the core assets of a top Hollywood studio.

What does this mean? Simply put, Netflix may be able to decide for itself whether a blockbuster movie will be released in theaters first or directly on streaming platforms; it can also plan new Harry Potter movies and spin-off series simultaneously to maximize the value of the IP.

For viewers, this might mean more high-quality content and a faster update pace. But for the industry ecosystem, it could have a profound impact.

Jin Ge believes that Disney's acquisition of Fox was a case of the strong getting stronger. Netflix, on the other hand, was forced to transform from a "pure streaming media" company into a "comprehensive entertainment company." "When Disney acquired Fox, it already had a huge content pool, as well as theme parks and consumer products businesses, so that acquisition was more like 'expanding its own universe by another dimension.' But Netflix is filling the gaps it lacks, such as large IPs that can be developed in a circular manner, global theater relationships, and a long-term copyright asset pool. Behind this is an upgrade of its business model, as well as a forced reality."

For viewers and subscribers, this could mean a more stable and abundant supply of blockbuster movies, or it could mean a further increase in the frequency and quality of content released on the Netflix platform in the future.

However, many industry insiders are beginning to worry: when content production, distribution, and streaming platforms are all concentrated in the hands of a single company, will the power of independent producers, low-budget films, and even theaters themselves be further squeezed? After all, Netflix has historically maintained a conservative stance on theatrical releases, preferring a "release-to-watch" model. If it ultimately becomes Warner Bros.' owner, will it continue this strategy? Or will it adjust its approach to maintain Warner Bros.' traditional theatrical relationships? These questions remain unanswered.

Furthermore, the merged entity will have a highly centralized ownership and profit distribution structure. When content, capital, and distribution are controlled by a few companies, industry competition and room for diversification may shrink, which is not good news for emerging producers, niche content, and independent films.

Even more alarming is the accelerating concentration of content resources on leading platforms. For Netflix, acquiring classic and contemporary hit IPs such as Harry Potter, DC Universe, Game of Thrones, Friends, and The Big Bang Theory represents a qualitative leap in its content library.

For its competitors, this means that high-quality content will become even more concentrated on a few top platforms. Acquiring popular IPs will become more difficult. In the long run, while viewers' choices may seem abundant, they may actually become increasingly similar, with everyone watching the "safe" options offered by the same few giants, while experimentation and diversity are sacrificed.

“Warner’s content won’t all be exclusively available on Netflix in the short term, but it might in the long term,” Jin Ge analyzed. “It won’t hurt viewers in the short term, but content prices will rise and platform differentiation will intensify, which is an inevitable trend.”

Netflix's indirect entry into China: Could it be leveraging theatrical releases to share in the Chinese box office boom?

Globally, this acquisition has reshaped the competitive landscape of the streaming industry.

Over the past few years, Disney+ has maintained its leading position with its IP portfolio of Disney, Marvel, Star Wars, and Pixar; Amazon Prime Video, on the other hand, relies on its massive e-commerce membership system to integrate film and television content as part of its ecosystem services; Apple TV+ takes a premium approach, offering a limited but high-quality selection.

Now, Netflix not only boasts a powerful global distribution network, but has also secured a deal with Hollywood's most prestigious content production company. It is no longer just a "technology company that only makes streaming media," but a true entertainment empire with a platform, production capabilities, and a library of classic IPs accumulated over decades.

In terms of overall strength, Netflix has become a true Hollywood giant and a global streaming platform.

So, what does this mean for the Chinese market?

While Netflix still cannot directly operate its streaming service in mainland China, its acquisition of Warner Bros. could potentially provide a "backdoor" entry. It's worth noting that Warner Bros. films have long been able to be released in Chinese theaters, with titles like *Dune*, *The Matrix*, and *Fantastic Beasts* achieving considerable box office success. Now, Netflix is the true controller behind these films.

In other words, the Hollywood blockbusters that Chinese audiences will see in theaters in the future may already be backed by Netflix. While the platform itself can't enter the Chinese market, the content has already been there. This approach of entering through content rather than the platform complies with Chinese regulatory requirements while allowing Netflix to share in the commercial rewards of the Chinese market.

“From a business perspective, this is indeed a roundabout way to enter the market,” Jin Ge believes. “The Netflix app is not available in mainland China, but Warner Bros. movies still go to theaters, and the box office revenue from mainland Chinese audiences will eventually go into Netflix’s account.”

According to his assessment, while mainland audiences' access to movies will not be significantly affected in the future, they may still find it difficult to watch TV series. "If these major IPs release spin-off series in the future, they will likely be exclusive to Netflix, and these parts may not be able to be broadcast in mainland China."

Furthermore, as its new owner, Netflix's decisions regarding global content investment will also influence Warner's future creative direction. If it believes the Chinese market still holds enormous potential, Warner may place greater emphasis on the preferences of Chinese audiences in its subject matter selection, co-productions, actor choices, and even promotional strategies. For Chinese cinemas, distribution companies, and content partners, they will be facing a "new Warner" with stronger capital, richer resources, and a more global strategy.

(Source: Daily Economic News)